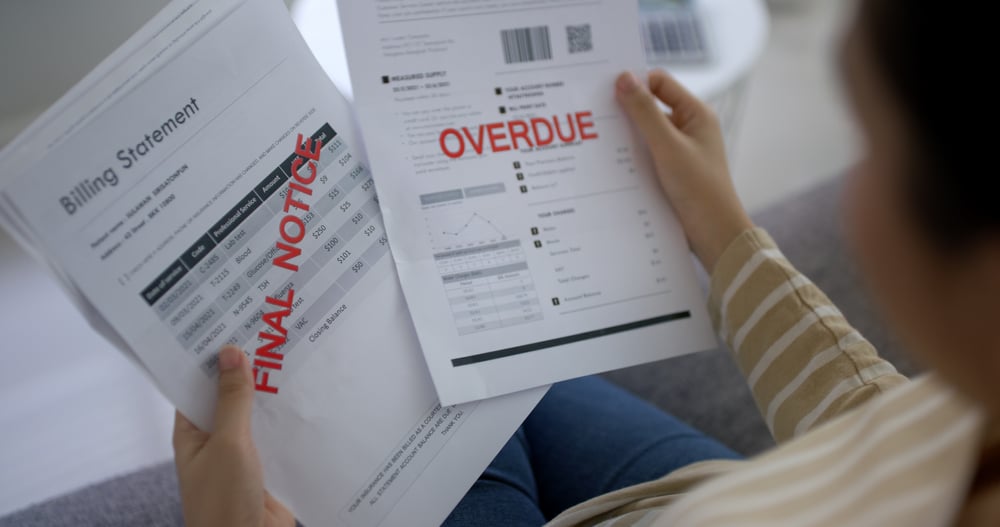

Consumers have been increasingly relying on credit cards to make ends meet, and it may be finally catching up with them.

The national average credit score, which has steadily increased over the last decade, fell to 717 from a high of 718 in the beginning of 2023, according to a report from FICO, developer of one of the scores most widely used by lenders. FICO scores range between 300 and 850.

“It’s a notable milestone,” said Ethan Dornhelm, FICO’s vice president of scores and predictive analytics. “This is the first time in well over a decade that the score went down.”

Average nationwide credit scores bottomed out at 686 during the housing crisis more than a decade ago, when there was a sharp increase in foreclosures. They steadily ticked higher until the Covid-19 pandemic, when government stimulus programs and a spike in household saving helped scores jump to a historic high in April 2023.

High-interest rates and higher prices have weighed on most Americans’ financial standing. Consumers as a whole are falling deeper into debt, causing an increase in credit card balances and an uptick in missed payments, FICO found.

As of October, the average credit card utilization was 35%, up from 33% a year earlier, and just over 18% of borrowers had a more than 30-day past-due missed payment against their credit accounts, up from 16.5% the year before.

“Another likely driver is that savings rates have trended back down to zero and those savings cushions that many consumers had have disappeared,” Dornhelm said.

During the pandemic, most Americans benefited from a few government-supplied safety nets, including the large injection of stimulus money. That left many households sitting on a stockpile of cash that enabled some cardholders to keep their credit card balances in check.

But that cash reserve is largely gone after consumers gradually spent down their excess savings.

“We are pretty far removed from pandemic-level mitigation programs, so consumers are very much confronted with making good on their credit obligations with little in the way of stimulus checks or government defined accommodation programs,” Dornhelm said.

{kind=link}